The bucket method—briefly mentioned during our visit to Budget Island—is a simple yet powerful way to assign your money to specific tasks. With a limited income, there are only so many directions we can steer our resources. While peace of mind and financial security are vital, so too are moments of joy and things to look forward to. Allocating your income into defined “buckets” allows you to balance these competing priorities and move forward with clarity.

Of course, your allocation depends on where you are in the game. Everyone’s situation is unique. A younger person might lean heavily into the social bucket—nights out, experiences, spontaneity—while someone approaching retirement will likely shift focus to stability and legacy. It also depends on your snapshot in time: are you in a position of relative ease, or feeling financially crushed?

At one end of the spectrum is debt slavery, where obligations feel suffocating and freedom seems distant. If that’s your reality, then zeroing in on debt reduction must take priority. Sacrificing short-term pleasure can be painful—but your future self will look back with gratitude for the hard-fought liberation.

At the other end is financial freedom—when your money works for you, earning enough to meet your lifestyle needs without eroding the principal. Most people fall somewhere in between, leaning closer to the debt-heavy side of the distribution. The bucket method offers a way to reframe progress: not as an all-or-nothing achievement, but as steady movement toward self-defined goals.

Buckets might include things like:

- Big bills – Putting a small amount aside over time ready for when large bills come due.

- Holiday Fund – for planned escapes and recharging.

- Practical Reserves – car replacements, home repairs, medical gaps.

The beauty of this method lies in its flexibility. If your income is predictable, you can allocate and automate with relative ease. If it’s sporadic, creativity is key—shifting priorities and flow as needed.

It’s tempting to create many buckets, and there’s nothing wrong with that—but bear in mind that more buckets mean more management. Thankfully, there are tricks to simplify things. Many bank accounts allow sub-account setups with scheduled transfers or “sweep” functions that move funds based on balance thresholds. Even small automation—like rounding up purchases to the nearest dollar and saving the difference—can quietly grow reserves in the background.

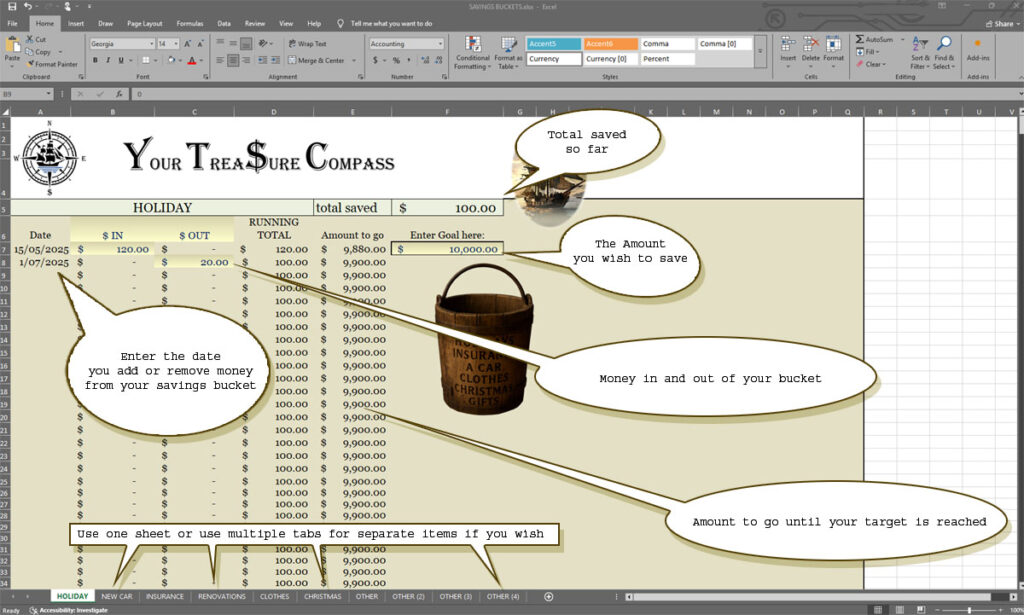

Although you can simplify things with separate bank accounts, this isn’t always possible. Your bank may not provide such an option, or you may find it better to keep your money in one account if it serves the purpose of reducing your mortgage payments. A redraw or offset facility would be such examples. In this case you can track your saving manually using a spreadsheet. Luckily you can download our free template form yourtreasurecompass.com.

Get Instant Access to Your Free Expense Tracker, Balance Sheet Templates & more

Just fill out the form below to download your templates.

If you’d like, you can opt-in for occasional updates, helpful reminders, or extra tools to help you stay on track.